Fortune Brands Home & Security, Inc. () seems to be a slightly undervalued player in the home improvement segment that has astutely chosen to work with market leaders Home Depot () and Lowe’s () instead of compete with them head-on. Market conditions being favorable to the giants in the segment, that effect is expected to cascade down to Fortune’s product lines as well. Valuation analyses show that the stock is trading slightly below intrinsic value after the January dip that also hit HD and LOW, which means some margin of safety for investors looking to get in now. Let’s look at the company’s market distribution, growth, acquisition and fiscal strategies and balance sheet strength to see if the company possesses enough firepower to leverage the market’s growth expectations for the next several years.

Fortune Brands is a leading home and security products company with products addressing niche segments within the home improvement market. The company operates four business segments: cabinets, plumbing, doors and security.

As most investors will know, the home improvement market in the United States is a highly mature one with two really strong players – Home Depot and Lowe’s – staying in control of the market. But, as a manufacturer, Fortune Brands works with them rather than against them, with each accounting for more than 10% of the company’s sales in fiscal 2017.

Source: 2017 Annual Report

Between 2012 and 2017 the company’s sales increased by more than 70%, from $3.13 billion to $5.28 billion. But the best part is operating margins more than doubled during the period. Additionally, international sales account for 15% of the company’s sales as of 2017, giving it further growth opportunities outside its core market.

Though a large part of the recent growth can be attributed to the steady stream of acquisitions during the period, the fact that operating margins kept increasing shows very clearly that the new businesses were a great strategic fit. What Fortune has been trying to do is to build brands that can serve customers at various price points. For example, Moen, ROHL, Perrin & Rowe are all differently positioned brands serving the plumbing segment.

Bolt-on acquisitions appear to be one of the key drivers for growth, and the company deployed approximately $1.5 billion on eight acquisitions during the period in question. It also returned $1.5 billion to shareholders in the form of share repurchases.

What allows the acquisitions to strengthen the core brands is market positioning. The company has a No. 1 product in every single category it operates in. As can be expected, these are all high-margin products sitting atop their respective niches. The table below shows you the kind of strong market presence and pricing power the company’s core products command.

Source: Investor Presentation

On the balance sheet front the company had $1.507 billion in long-term debt at the end of fourth quarter of 2017, while cash on hand was $323 million. Interest expense and dividends paid for the full year were $49.4 million and $110.3 million, respectively. Operating income for the fiscal was $692 million.

Those numbers call out Fortune’s ability to raise more debt for key acquisitions as well as to keep increasing dividends over the medium term.

Leveraging Macro Trends

The company is clearly well managed, not only from a financial perspective but operationally as well. With strong fundamentals in place, Fortune is well positioned to take advantage of the two important drivers of the home improvement industry: The U.S. economy and the age of U.S. housing stock.

In a recent article on Home Depot called 2 Things Will Prolong Home Depot’s Impressive Growth, I wrote about the ability of these two factors to help companies like Home Depot show sustained growth over the next several years. That, obviously, applies to Fortune as well, as a manufacturer of number one branded home and security products.

Here are some key points from that article:

-

Inflationary indices are expected to stay stable through 2022.

-

The median age of homes in the U.S. went from 31 years-plus in 2005 to 37+ years in 2015 to the current 40 years-plus.

-

The increasing median age “signals a growing market” for remodeling as well as new construction, according to the National Association of Home Builders.

These macro trends will positively impact the entire industry, lifting companies like Fortune that are well positioned to take advantage of them.

Valuation

Source: Free Cash Flow – Morningstar, Other data from company filings

Valuation analyses using Ben Graham’s intrinsic value and discounted cash flow models show that the market expects the company to grow at a 4% rate long term. That’s a reasonable expectation considering the strength of the company’s balance sheet and how strongly its acquisitions have been accretive to growth and operating margins.

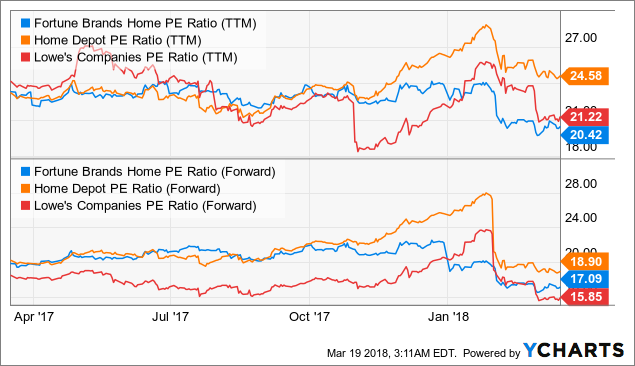

FBHS PE Ratio (TTM) data by YCharts

FBHS PE Ratio (TTM) data by YChartsThe current PE ratio of 20 times earnings and 17 times forward earnings also bear out the fact that FBHS is trading at reasonable multiples, and with some margin of safety for investors at the current price level of around $62. Considering all factors, the price dip since January seems to have opened a nice window of opportunity to add to or open a position.

Disclosure:I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source

http://seekingalpha.com/article/4157649-fortune-good-opportunity-home-improvement-niche